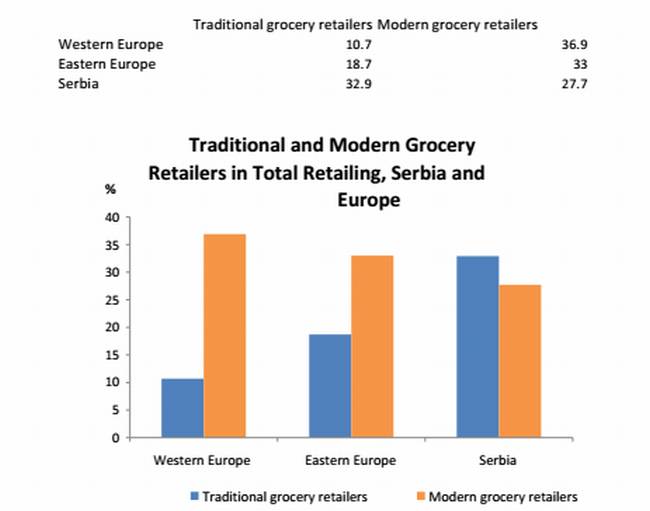

Retailing in Serbia is lagging behind Western Europe and even to Eastern European region; this situation is obvious to both experts and laymen. For example, according to Euromonitor International’s, traditional grocery retailers account for 11% of retailing in Western Europe, which is a decline compared to 2008, when it had stood at 12%. In Eastern Europe, traditional grocery retailers claim 19% in 2013, while they had been accounted for 23% in 2008. In Serbia, however, this channel value went down from 41% in 2008 to 33% in 2013. In the same time span, modern grocery retailers jumped from 35% to 37% in Western Europe, from 27% to 33% in Eastern Europe and from 19% to only 28% in Serbia. The performance of traditional grocery retailers and modern grocery retailers can certainly be taken as one the best indications that retailing in Serbia is underdeveloped. However, one can’t deny that it is slowly catching up and following the footsteps of more developed nations’ retailing landscape.

There are several trends shaping the development of grocery retailing in Serbia and among the most important are certainly convenience and market consolidation. Convenience trend is partly responsible for persistent popularity of traditional grocery retailers in Serbia due to the fact that these retailing outlets, especially very popular independent small grocers, offer superior proximity and extended opening hours to consumers, not to mention the human warmth of doing a daily purchase in a neighboring store where the owner and his family members are usually the only employees and everybody know them very well.

Even though it might seem paradoxical at a first glance, the convenience trend is also driving the growth of modern grocery retailers. Namely, more and more convenience stores are being opened in densely populated urban areas of Serbian cities and their market share within Serbian retailing grew from 4% in 2008 to 5% in 2013. Convenience is also driving the development of smaller supermarkets that are rapidly increasing in number as well. The value share of supermarkets in Serbia went from 9% of total retailing in 2009 to 12% in 2013.

Another important trend within Serbian retailing landscape is market consolidation. We witnessed several major events in this area in last several years. Firstly Delhaize Group took over Delta Maxi doo, then Mercator purchased Familija and Agrokor Group took over Tuš. Finally, long-expected acquisition of Mercator by Agrokor Group has occurred in June 2013 and this rounds up Serbian retailing system as a duopoly.

We expect to see more international chains entering the market in next five years. Just how much the consolidation is reshaping retailing in Serbia and jeopardizing traditional grocery retailers can be seen from the fact that Serbian Traders Association (Udruženje trgovaca Srbije – UTS) was founded in the end of 2010 with the aim to protect and represent small retailers’ interests. However, this is not likely to significantly slow down the modernization of Serbian retailing. On the contrary, Euromonitor International expects to see number and market share of modern grocery retailers, especially large formats such as supermarkets and hypermarkets, growing together with emerging trends among Serbian consumers of doing weekly or even monthly purchases in huge retailing centers.

Milan Cakić, Contributing Analyst at Euromonitor International